Table of Contents

What happened and why buyers should care now

On February 20, 2026, the White House issued a proclamation imposing a temporary 10 percent ad valorem import surcharge under Section 122 of the Trade Act of 1974. The Section 122 10% import surcharge 2026 took effect at 12:01 a.m. eastern time on February 24, 2026, and the proclamation says it runs through July 24, 2026, unless it is ended earlier or extended by Congress. For U.S. power plant, grid, EPC, and industrial buyers, that is not just a trade headline. It is a landed cost problem, a planning problem, and in many cases a contract risk problem. Understanding the implications of the Section 122 10% import surcharge 2026 is crucial for effective procurement.

Businesses importing goods into the U.S. should stay informed about the Section 122 10% import surcharge 2026 and how it may affect customs duties and pricing.

This article is written for procurement managers, sourcing leads, expeditors, project directors, compliance staff, and owner-side engineers who buy routine but critical industrial items. It will educate them on Section 122 10% import surcharge 2026. Think about valve actuators, instrumentation, bearings, gaskets, specialty fasteners, electrical accessories, enclosure hardware, fittings, low-value emergency spares, and repeat MRO lines. Many of these are not glamorous purchases, but they are exactly the kind of items that can quietly break budget, delay a shutdown, or create internal blame when a new surcharge appears after the quote is already approved.

The Section 122 10% import surcharge 2026 could lead companies to reassess supplier relationships and explore alternative sourcing options.

The key point is simple. Do not assume your shipment is safe because it is small, urgent, or related to power generation. The official text creates exceptions for certain categories, but it does not create a broad exemption just because the end use is a power plant. That is why buyers need to read the rule by product treatment, not by project importance.

Importers should closely monitor policy updates related to the Section 122 10% import surcharge 2026 to avoid unexpected duty increases and ensure accurate landed cost planning.

The official rule in plain English

As the deadline approaches, it’s essential for buyers to stay informed about the Section 122 10% import surcharge 2026 and its potential impact on their operations.

After the Section 122 10% import surcharge 2026, the White House proclamation says all articles imported into the United States are subject to a 10 percent ad valorem duty unless an exception applies. It also says the surcharge is in addition to other duties, taxes, fees, exactions, and charges, except that it does not apply in addition to Section 232 tariffs on the portion of an import already covered by Section 232. The proclamation also says the surcharge is treated as a regular customs duty.

Experts suggest that planning ahead for the Section 122 10% import surcharge 2026 can help importers avoid unexpected cost increases.

For busy buyers, that means three practical questions must now sit beside every quote review. First, does the product fall into an exception category? Second, is any part of the item already under Section 232 treatment? Third, has your customs broker confirmed the HTS treatment and entry plan before shipment leaves the foreign supplier? If your team cannot answer those three questions, you are not ready.

10% import surcharge 2026: What is exempt and what is not

Official sources list category based exceptions. The fact sheet names certain critical minerals, metals used in currency and bullion, energy and energy products, certain natural resources and fertilizers, certain agricultural products, pharmaceuticals and pharmaceutical ingredients, certain electronics, certain vehicles and certain parts, and certain aerospace products. The proclamation also states that goods already under Section 232 treatment are not charged the Section 122 surcharge on the portion already covered by Section 232. It also exempts qualifying duty free goods of Canada or Mexico under the USMCA terms stated in the proclamation.

With the potential introduction of the Section 122 10% import surcharge 2026, many logistics teams are updating their compliance and budgeting strategies.

This is where buyers make expensive mistakes. They hear that energy and energy products are excepted and then assume plant equipment is also exempt. That is not the same thing. Fuel, energy products, and some upstream categories can be excepted. But many ordinary plant spares and industrial components are still only exempt if their specific tariff treatment falls inside the official exception structure. After the Section 122 10% import surcharge 2026, a valve positioner, a set of bearings, a control cable accessory, or an emergency actuator repair kit may still be exposed.

No blanket power plant exemption

If the item is going into a gas turbine site, substation, thermal plant, LNG terminal, or grid project, that end use alone does not automatically remove the surcharge. For the Section 122 10% import surcharge 2026, the safer reading is this: check the tariff treatment first, then verify whether the product fits an exception, a Section 232 overlap, or a specific special treatment. Project urgency does not change the customs result.

The three biggest cost traps for USA industrial buyers

1. Quoting without surcharge review

After the 10% import surcharge 2026, a supplier may still quote using old assumptions. If your RFQ, offer comparison sheet, or internal approval note does not state who owns new duty exposure, the company often absorbs the surprise later. On low-value shipments the hit looks small, but on repeat lines or shutdown buying it compounds fast.

2. Confusing end use with tariff treatment

Many teams speak in project language such as power plant spare, emergency maintenance item, or federal job support part. CBP entry does not clear by those labels. It clears by classification, declared value, origin, documentary treatment, and any applicable special measure.

3. Weak broker handoff

Buyers sometimes send the broker only the invoice and packing list after goods are already moving. That is too late for a rule change like this. The broker should see the product description, HTS logic, country of origin statement, any Section 232 issue, and the commercial context before departure when possible.

Many importers are closely monitoring the Section 122 10% import surcharge 2026 because it could significantly increase the cost of bringing goods into the United States.

How 10% import surcharge 2026 affects routine power plant and EPC buying

For your target market, the biggest exposure is not always large turbine packages. It is the repeated industrial consumable and small capital support lines that move under pressure. Examples include actuators, repair kits, cable glands, terminal accessories, panel hardware, control fittings, process instrument spares, specialty seals, couplings, and urgent mechanical parts sourced cross border because domestic lead time is poor or pricing is too high.

Understanding the regulatory details behind the Section 122 10% import surcharge 2026 will be important for importers who want to remain competitive in global trade.

These are exactly the items that create argument inside a plant organization. Procurement says the supplier did not warn us. Operations says the spare was urgent. Finance says landed cost was not approved. Engineering says the item cannot be delayed. The new surcharge makes this worse because it adds one more variable to already compressed buying decisions.

If implemented, the Section 122 10% import surcharge 2026 may affect small businesses that rely heavily on overseas suppliers for raw materials and finished products.

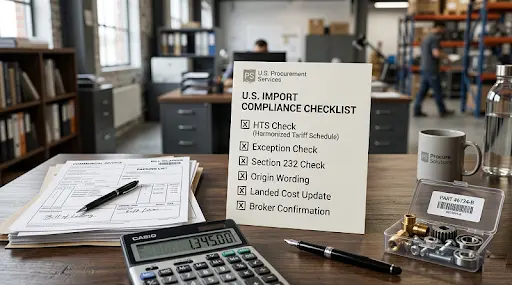

The short list buyers should check before release

Use this as a pre-shipment control list for any industrial line exposed to the new rule.

- Confirm the current HTS classification with your customs broker or trade counsel where needed.

- Check whether the item fits any official exception category, and do not rely on informal assumptions.

- Review whether any portion of the item is already subject to Section 232 so you do not double count the duty.

- Confirm country of origin wording is consistent across invoice, packing list, and any supplier declaration.

- Update landed cost before management approval, not after goods are on the water or in the air.

- State in the purchase order who bears new tariff or surcharge exposure if a rule changes between quote date and entry date.

- Keep a shipment file with the broker note, classification logic, source documents, and internal approval trail.

Trade analysts believe the Section 122 10% import surcharge 2026 could encourage companies to reconsider their global sourcing strategies.

What smart USA buyers should do this week

Refresh your RFQ and PO language

Include a short but important clause in your supplier agreements. Ask suppliers to confirm that their quoted pricing reflects all known duties and temporary surcharges in effect on the quote date, including the 10% import surcharge 2026, and require them to disclose any product classification or country-of-origin assumptions used in their pricing. While this will not eliminate every potential dispute, it ensures greater transparency and forces key cost assumptions to be clarified early in the process.

Create an exception review step

For power plant and grid buyers, one page is enough. Build a mini review sheet with item description, HTS code, supplier country, stated origin, possible exception, Section 232 check, and broker confirmation date. When done consistently, this saves far more money than it costs.

Separate urgent spare buying from blind spare buying

Urgent purchasing is common in industrial operations, but blind buying should never be the response. When a production line is time-critical, the procurement process needs tighter control, not fewer checks. Rapid shipments increase the risk of unexpected costs, especially with policy changes like the 10% import surcharge 2026. That is why pre-clearance planning, accurate classification, and confirmed landed costs become even more important when speed matters most.

Keeping the Conversation Practical for Industrial Buyers

Urgent purchasing is common in industrial operations, but blind buying should never be the response. When a production line becomes time-critical, the procurement process must become more controlled, not less. Rapid shipments increase the risk of unexpected landed costs, especially when policy changes such as the 10% import surcharge 2026 can suddenly affect imports. This is why pre-clearance thinking—verifying classification, origin assumptions, and total landed cost—becomes even more important when speed matters.

FAQ

Yes. The White House proclamation says the 10 percent temporary import surcharge became effective at 12:01 a.m. eastern standard time on February 24, 2026.

The proclamation states it continues through 12:01 a.m. eastern daylight time on July 24, 2026, unless it is suspended, modified, or terminated earlier, or unless Congress extends the period.

No. The official sources describe category based exceptions. They do not create a blanket exemption simply because an item will be used in a power plant or grid project.

The proclamation says the Section 122 surcharge does not apply in addition to Section 232 tariffs on the portion of an import already covered by Section 232.

Not always. The proclamation says articles entered free of duty as goods of Canada or Mexico under the stated USMCA terms are excepted. Qualification still matters.

Confirm HTS treatment, check the exception logic, review origin language, update landed cost, and get broker confirmation before goods depart when possible.

Conclusion

Understanding how the Section 122 10% import surcharge 2026 applies to different product categories will be essential for importers planning their logistics and budgets.

The changing trade landscape means industrial procurement can no longer rely on simple price comparisons. With policies like the Section 122 10% import surcharge 2026, even small regulatory shifts can quickly affect margins, timelines, and supply chain decisions. For U.S. power plant and EPC buyers, the smartest approach is not panic but preparation. Review tariff classifications, confirm eligibility for exceptions, document your assumptions, and ensure the full landed cost is clear before moving any shipment. Staying proactive about the Section 122 10% import surcharge 2026 helps buyers protect budgets, avoid customs surprises, and maintain control over project timelines.

At shafiqulmowla.com, we want to win trust with U.S. readers. We are specific, and practical. We avoid legal overclaiming.